931.905.0050

931.905.0050

A tale of two economies

January 23 – 27, 2017

“This American carnage stops right here.”

– Donald Trump, Inaugural Address

“The Fed’s goal is to promote financial conditions conducive to maximum employment and price stability… So where is the economy now, in relationship to them? The short answer is, we think it’s close.”

– Fed Chair Janet Yellen, January 18

It goes without saying that there is a sharp contrast between the economic views of the incoming administration and those of the Federal Reserve. President Trump, and most of the individuals who voted for him, sees a weak economy, devastated by job losses in manufacturing. The Federal Reserve sees an economy nearing full employment. So who’s correct?

Most economists will tell you that we are in a “new normal,” defined largely by demographic changes. In the final decades of the 20th century, labor force growth was boosted by the entrance of the baby-boom generation into the workforce and a rising trend of female labor force participation. Those trends are well behind us, and the labor force is currently growing at about a third of the pace seen between 1960 and 2000 (slower labor force growth is a worldwide phenomenon). Hence, unless we see a sharp rise in immigration or a unprecedented increase in productivity growth, real GDP growth will be a lot slower than a few decades ago (1.5-2.0%, rather than 3.0-3.5%).

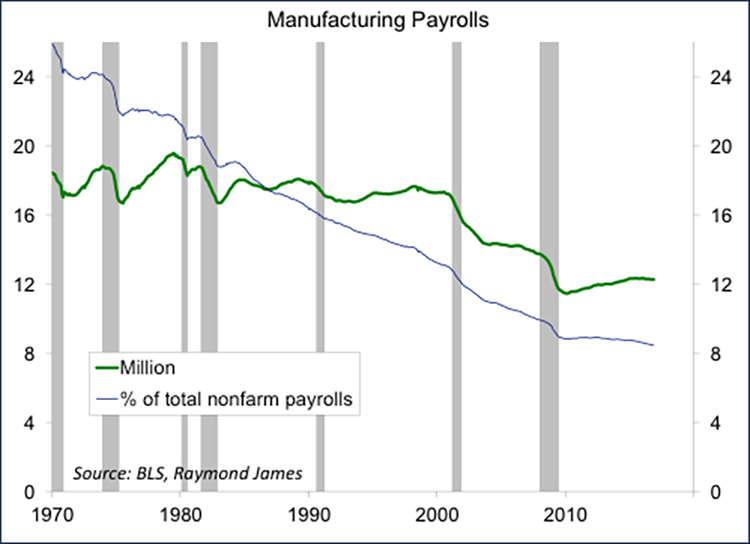

The trend in manufacturing employment was roughly flat between 1960 and 2000, but that masked a lot of flux in the sector. Factory jobs have always come and gone, but manufacturing output has increased substantially over the years. The number of manufacturing jobs dropped in the last two recessions, but failed to rebound as they had in past recoveries. Foreign trade, particularly with China, has been a factor, but it’s estimated that about half of the factory job losses have been due to technology improvements (robotics).

Note that much of the increased trade with China came at the expense of other Asian nations. China appeared to be manipulating its currency about 10-15 year ago, weakening it to encourage export growth. However, that’s not the case now. China is actively trying to prevent its currency from weakening.

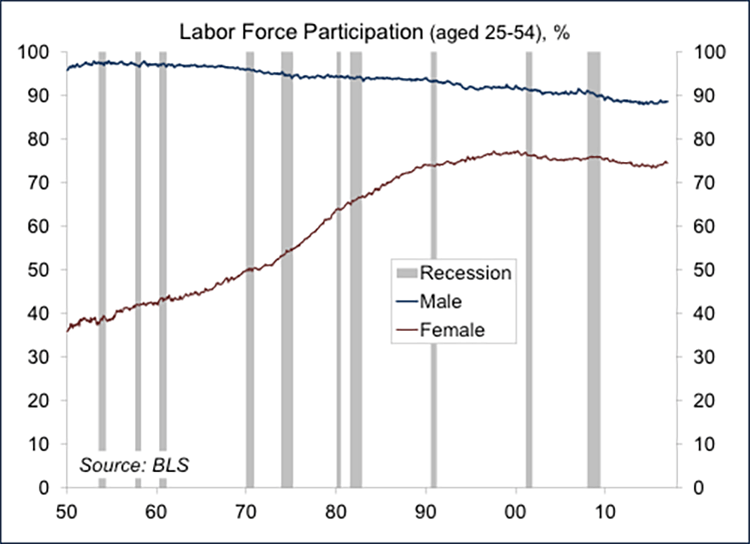

Labor force participation is down since the recession, but much of that is demographics. Increased school enrollment has reduced participation for young adults, while the baby-boom generation is now edging into retirement.

The decrease in participation for prime-age males is a long-term trend. Nearly half of this group is reported to be in poor health and is taking pain medication (and about 40% indicate that this is preventing them from working). Higher wages and increased healthcare could help lift participation for this group, but the upside is likely limited in the short term. Participation for prime-age females has declined in the last two decades, likely reflecting better benefits (maternal leave, etc.) and better wages (which facilitates them taking more time off).

The tools of monetary policy are blunt. They can’t create great conditions for all regions and industries. Policymakers must focus on the bigger picture. The job market is getting tighter. Most Fed officials believe that we are close to full employment. Businesses are reporting greater difficulty in finding qualified workers, especially for skilled positions. Wage pressures are building. There is considerable uncertainty about the character, timing, and size of fiscal stimulus. However, Federal Reserve officials believe they have plenty of time to respond as the outlook becomes clearer.

Contrary to the election-year rhetoric, President Trump has inherited an economy that is in good shape, with growth close to its limits. Faster economic growth is still possible. However, that will depend on boosting the pace of productivity growth. That should be the policy focus in Washington.

Thrill or chill on Capitol Hill?

January 16 – 20, 2017

Since the November election, the financial markets have priced in a more friendly business environment, with growth boosted by expansionary fiscal policy. However, the White House does not have absolute power. Congress writes the laws. While the outcome is uncertain, the legislative mechanics suggest that may see little, if any, tax cuts in calendar 2017.

With Republicans controlling the White House and both chambers of Congress, many see this as their best chance for tax reform. The House Speaker Ryan’s “Better Way” plan is expected to be the general blueprint for tax reform, but there will surely be many modifications along the way.

How will tax cuts be achieved, legislatively? The House of Representatives requires a simple majority vote. The journey through the Senate is more complicated.

The first possible path is through a tax reform bill, which would require 60 votes in the Senate. While that seems unlikely, given that the Republicans have only a 52-48 majority, it is not impossible. Republicans would have to get eight or more Democratic senators on board. A compromise plan would likely have smaller tax cuts than is currently anticipated, weighted toward large corporations, not small businesses and individuals. We would expect to see some change in tax rates for overseas earnings as part of the package.

The other Senate path is through budget reconciliation, which would require a simple majority (51 votes). The Senate would pass a budget resolution with reconciliation instructions, then develop legislation that comports to those instructions. However, the Senate can do only one set of reconciliation instructions per calendar year, and this year that set of instructions will be on repealing and replacing the Affordable Care Act. The Senate could add tax reform instructions in the budget resolution this year for calendar 2018, which means that tax cuts would occur next year. Note that the Affordable Care Act was paid for partly by higher taxes, and those increases may be jettisoned in healthcare reform (although it’s unclear what sort of replacement we may see in the months ahead).

The Senate is also subject to the Byrd rule. During the reconciliation process, a piece of legislation may be blocked if it increases the federal deficit beyond a ten-year window. This explains why the Bush tax cuts were not made permanent at their inception (changes would have to sunset to make the long-term numbers work out). This led to a series of extensions, until a compromise solution was reached.

Tax simplification should be a part of tax reform, and the elimination of many deductions would be expected to offset some of the cost of reducing tax rates. Steve Mnuchin, the Treasury Secretary nominee has said that tax reform will be revenue neutral, but that seems doubtful based on the numbers proposed during the campaign.

There are a large amount of tax deductions in the current law. Also called “tax expenditures,” these deductions totaled about $1.5 trillion in 2016 (vs. total tax receipts of $3.3 trillion) or about 8% of Gross Domestic Product. Early drafts of the tax reform plan would likely call for the elimination of many deductions, with the exception of (for individuals) the mortgage deduction and charitable contributions, and (for businesses) research and development. In the past, scaling back tax breaks has been extremely difficult, so we’re unlikely to see much change as tax legislation nears its final form.

Still, even if we don’t get the amount of tax cuts that the financial markets are hoping for, reduced regulation ought to create a more business-friendly environment. The first principle of regulation and enforcement is that principals matter. That is, priorities, effort, and direction flow from those in charge. For the financial sector, we are going to see a complete change in regulatory leadership in the next year and a half.

At the Fed, Janet Yellen’s terms as chair runs to February 3, 2018. At this point, it appears unlikely that President Trump will re-nominate her. She could stay on as a Fed governor (which runs to early 2024), but that is unlikely. Stanley Fischer’s term as vice-chair runs to June 12, 2018, and he would likely leave when Yellen does (his term as governor runs to early 2022). For the last year and a half, there have been two vacancies on the Fed’s Board of Governors. The Fed has taken on a greater supervisory role since the financial crisis, but the vice-chair for regulation has remained vacant. Governor Tarullo has served in that capacity, but is expected to leave if that slot is filled. Hence, the incoming president will be able to shape the Fed’s Board of Governors to his choosing.

Following the election, market participants have been enthusiastic about the possibility of a large infrastructure spending program. The view that this will be funded mostly through the private sector (as per Trump’s proposal) gained further credence following Elaine Chao’s hearing for Transportation Secretary. However, we still don’t have any details regarding how that is supposed to work, especially for rural areas needing transportation projects.

In short, post-election optimism is likely to turn to considerable second-guessing about priorities in Washington. Trump-transition people have suggested that there are no priorities. They will try to do everything at once. However, that’s not how Congress works. A new president normally enjoys a honeymoon period with Congress, but the Washington sausage factory is going to be interesting to watch.

December jobs report: Where to now?

January 9 – 13, 2017

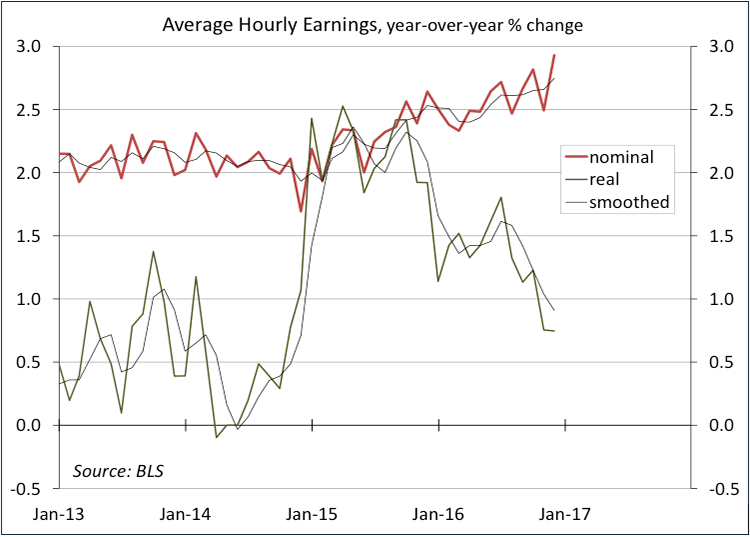

The December Employment Report showed the job market to be in good shape. The pace of job growth slowed in 2016, partly reflecting tighter labor market conditions. The unemployment rate edged up, following an unusually large drop in November. It’s unclear how much slack remains in the job market, but tight conditions should lead to faster wage growth. Average hourly earnings rose 0.4% (+2.9% y/y) in December. These figures tend to be choppy (the three-month average was up 2.7% y/y). While the job market news has remained good, there is more uncertainty as investors try to gauge the size and timing of fiscal policy changes and how the Federal Reserve will respond.

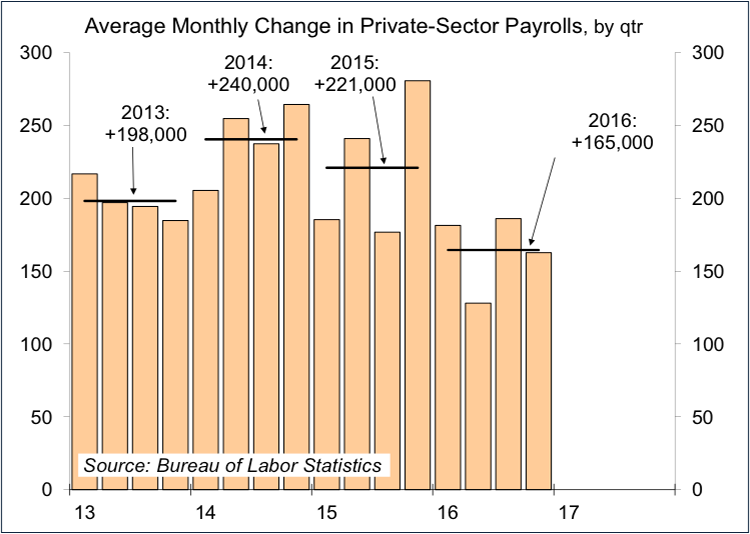

Annual benchmark revisions to the establishment survey data are due in February, but early indications are that the story is unlikely to change much. Private-sector job growth slowed in 2016, while government payroll growth has picked up somewhat. Hiring at small firms was strong in 2014 and 2015, a healthy sign for the economy. However, the ADP Employment Report suggests that hiring at small firms has slowed in recent months, offset partly by a pickup in hiring at larger firms.

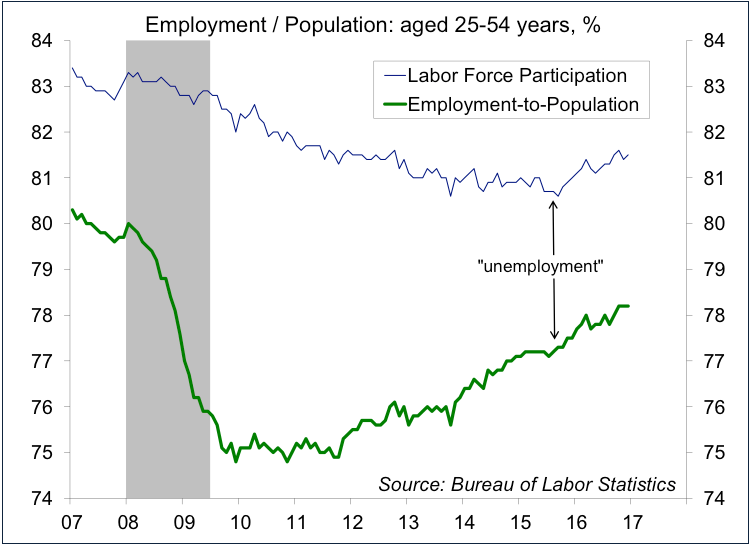

While job growth has slowed, it’s still beyond a sustainable pace (that is, stronger than would be consistent with the growth in the working-age population). As a consequence, the unemployment rate has declined. However, there are potential workers on the sideline – not officially counted as “unemployed,” but willing to take a good job if available. At this point in the cycle, the unemployment rate ought to level out as these workers return to the labor force. Labor force participation and the employment/population ratio have been little changed over the last year, but improvement is clearer for the key age cohort (those aged 25-54). As members of this key age cohort move into better jobs, opportunities should open up for younger workers. We still have some way to go before we are at full employment, but we are on our way.

As the job market tightens, wages will be bid up. Average hourly earnings rose at about a 2.0% annual rate in 2013 and 2014, picking up to 2.5% in 2015. While the monthly wage figures are uneven, the trend in wage inflation appears to be gradually higher. Note that while nominal (current dollar) wage growth has picked up, real (inflation-adjusted) wage growth has slowed relative to a year ago. But while real wage growth, the key driver of consumer spending, has slowed, it remains moderately strong by historical standards.

The labor market is the widest channel for inflation pressure. The Fed’s inflation hawks (mostly district bank presidents, not all of whom vote on monetary policy) worry that firms will pass higher costs along, and are more inclined to raise short-term interest rates sooner. The moderates (including Chair Yellen) seem willing to err on the side of waiting a little too long.

The Fed policy outlook is clouded by the uncertain outlook for fiscal policy (timing, magnitude), but the Fed will respond to the economic implication of policy changes in Washington once they occur. Uncertainty should be a major factor for the markets.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report’s conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.